What you need to know about Medicare

Medicare can be complex. This information is here to help make it clearer, so you can feel confident choosing the plan that's right for you.

The four parts of Medicare and what they cover

Medicare is made up of four parts. Two of those parts are sponsored by the federal government and two refer to plans you can get from private health insurance companies.

Medicare Part A: Hospital Insurance

Part A covers:

- Up to 150 days in the hospital

- Up to 100 days in a skilled nursing facility (after a qualifying three-day hospital stay)

- Home health care

- Hospice care

You're responsible for: deductibles, copays and coinsurance.

Medicare Part B: Medical Insurance

Part B covers:

- Doctor visits (for regular screenings, vaccines, annual wellness and illnesses or injuries)

- Outpatient surgery (when you have surgery and go home the same day)

- Ambulance (if you have an emergency and an ambulance brings you to the hospital)

You're responsible for: monthly premiums, deductibles, copays and coinsurance.

Gaps in Original Medicare

Original Medicare covers a lot, but it doesn't pay for all the health care you may need. If you only have Part A and Part B coverage, you'll pay the full cost for services Original Medicare doesn't cover, including:

- Routine dental care

- Hearing aids

- Routine eye exams and eye wear

- Routine physical exams

- Fitness club memberships

- Prescription drugs you may take at home

- Care in a skilled nursing facility without a qualifying three-day hospital stay

- Most care you receive when traveling outside the U.S.

Medigap plans

If you choose Original Medicare, you can buy extra coverage from private insurance companies to help pay for things that Medicare Part A and Part B don't cover. Medigap plans cover things like coinsurance and copays, deductibles, your share of extended hospital stays and hospice costs, blood transfusions, and foreign travel emergencies.

Part C is also known as Medicare Advantage. These are private plans that cover everything Original Medicare does plus prescription drugs and other extras.

Medicare Advantage plans cover:

- Everything original Medicare covers

- Extras like vision, dental, over-the-counter items, hearing aids and fitness benefits (depending on the plan)

- Part D prescription drug coverage

You're responsible for: monthly premiums, deductibles, copays and coinsurance.

You can purchase Part D coverage from private health care companies to help cover the cost of your prescriptions. There are two ways to get Part D:

- As part of a Medicare Advantage plan (MA-PD)

- As a separate, standalone prescription drug plan (PDP)

Part D covers:

- Prescription drugs you take regularly or for an illness or injury as long as they are on your plan's drug list or formulary. Drug lists vary by plan, so it's important to check that your prescriptions are included before you pick a plan.

You're responsible for: monthly premiums, deductibles, copays and coinsurance.

A note on penalties

You don't have to get a Part D plan when you enroll in Medicare. But if you don't sign up when you first become eligible, you may pay a late enrollment penalty if you decide to sign up later. You'll pay the penalty for as long as you have Part D coverage. To learn more about penalties related to Part D enrollment, visit the Medicare website.

Phases of Part D coverage

Part D coverage is broken into phases. In general:

In the initial phase, you'll pay any deductible and coinsurance specified in your plan. Once you reach $2,100 in out-of-pocket costs for covered drugs, you enter catastrophic coverage. During this period, you pay $0 for covered drugs for the rest of the calendar year.

When to enroll in Medicare

Most people are eligible for Medicare at age 65. If you're already receiving Social Security benefits, you'll be enrolled automatically.

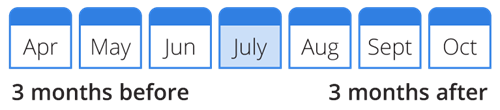

If you're not receiving Social Security benefits, you'll need to sign up for Medicare. You have seven months to sign up for Medicare — three months before your 65th birthday, the month of your 65th birthday, and three months after your 65th birthday.

Example: Your birthday July is 4

A note on delaying enrollment

You can wait to enroll if you plan to keep working and have coverage through your employer or your spouse's employer.

How to enroll in Medicare

You can sign up for Medicare three ways:

- Online at ssa.gov

- By phone at 1-800-772-1213

- In person at a Social Security Office

Getting a Medicare Supplement (Medigap) or Medicare Advantage plan

Once you're enrolled in Original Medicare, you can decide to enroll in a Medicare Supplement or Medicare Advantage plan from a private insurance company.

In addition to these time frames, there are special circumstances in which you can enroll or make changes. For example, if you were covered by your employer’s plan and didn’t enroll during the Initial Enrollment Period or you moved to a new area with different plan options.

For all of the details on enrollment guidelines and requirements, visit medicare.gov.

Medicare FAQs

Over the years, we've heard a thing or two from Medicare shoppers. We've compiled answers to a list of some common questions we hear.